No-Claims Bonus: The 8 Mistakes That Wipe It Out Instantly

.jpg)

Have you ever felt that rush of relief when your car insurance renewal drops because of your no-claims bonus? It's like a pat on the back for safe driving. But in 2025, with average UK car insurance premiums hitting £551 for the third quarter, that bonus could be your lifeline to affordability. Imagine saving up to 60% on your policy just by avoiding claims for a few years. Yet, one slip-up, and poof—it's gone. I remember advising a client in London who lost five years of bonus after a minor fender-bender he claimed on. His bill jumped £300 overnight. As a UK insurance expert with over 15 years helping drivers navigate this maze, I've seen too many folks torpedo their savings without realizing it. This hidden crisis is real: with premiums finally dipping after peaks in 2023, losing your NCB now hurts more than ever. Why risk it? Let's dive into the eight mistakes that can wipe out your no-claims bonus instantly, plus tips to safeguard it. Stick around; your wallet will thank you.

Understanding No-Claims Bonus: Your Ticket to Cheaper Cover

First off, what exactly is a no-claims bonus, or NCB as we insiders call it? It's that sweet discount insurers give you for each year you drive without making a claim. Think of it as a loyalty reward for being accident-free. In the UK, it builds up over time, often starting at 20-30% off after one year and maxing out at 60-70% after five or more. For example, a driver with 10 years NCB might pay just £404 annually, compared to £932 for someone with only one year. But here's the catch: it's not automatic, and it's fragile. Lose it, and your premiums could soar by hundreds. Why does it matter in 2025? With costs finally easing to around £400-£757 on average, depending on who you ask, that bonus is your buffer against inflation and rising repair bills. Don't let common pitfalls rob you of it.

How NCB Builds and Saves You Money

Your NCB accrues per policy, not per car, so it follows you when you switch insurers—as long as you have proof. Most companies cap it at nine years, but the savings compound. Ever wondered if it's worth protecting? Absolutely, especially if you've got three or more years stacked up. Protection add-ons, costing £20-50 extra, let you keep your bonus even after a claim. Without it, a single fault claim could knock off two years or more. It's like insurance for your insurance savings.

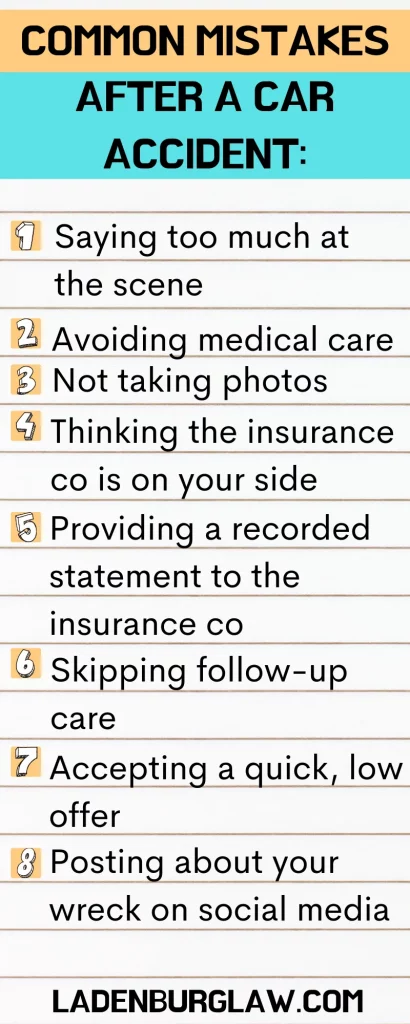

The 8 Mistakes That Can Wipe Out Your NCB Instantly

Now, the meat of it. These aren't rare blunders; they're everyday oversights that catch even seasoned drivers off guard. I've pulled from real cases and industry insights to highlight them. Avoid these, and you'll keep that bonus intact.

1. Claiming for Minor Damage You Could Pay Out-of-Pocket

Why claim for a £200 dent when it could cost you £500 in lost discounts? Small claims often aren't worth it, as they reset or reduce your NCB. I had a client who claimed for a scratched bumper—lost three years' bonus and regretted it instantly. Always crunch the numbers first.

2. Not Protecting Your NCB Add-On

Skipping NCB protection is like driving without a seatbelt. One at-fault claim, and you could lose all your accumulated years. Protection lets you claim once or twice without penalty, but many forget to add it at renewal. Question: Is £30 extra worth peace of mind? You bet.

3. Providing Incorrect NCB Information on Your Policy

Honesty is key. Declaring nine years when you have seven? That's fraud, and it voids your policy, wiping your real NCB too. A Reddit tale from 2025 shows a driver facing cancellation over this mix-up. Double-check your proof before submitting.

4. Letting Your Policy Lapse for More Than Two Years

Life happens—you sell your car, move abroad. But if you're uninsured for over two years, your NCB expires. One forum user learned this the hard way after a two-year break, starting from zero. Keep a cheap policy on a SORN'd car if needed, but beware: some say it doesn't count.

5. Adding a Named Driver Who Makes a Claim

Sharing your policy with a spouse or kid? If they crash and claim, it hits your NCB unless protected. Anecdote: A dad added his teen son, who had a minor prang—bye-bye to five years' savings. Vet named drivers carefully.

6. Assuming Non-Fault Claims Won't Affect You

Non-fault accidents should be recovered from the other party, but if not, it counts against you. Many lose bonus points here, thinking "it wasn't my fault" shields them. Insurers record it until resolved.

7. Switching Insurers Without Proper NCB Proof

New company? Send your NCB certificate within weeks, or they might cancel the discount. I've seen policies backdated with higher premiums over missing paperwork. Keep records handy.

8. Claiming for Windscreen Repairs Without Checking

Some policies treat windscreen claims as non-impacting, but others don't. A quick chip fix could ding your bonus if not specified. Always confirm with your insurer first—better safe than sorry.

Original Insight: Predicting NCB Trends for 2026

Here's my take as an expert: With EV adoption surging in the UK, by 2026, mistakes involving new tech—like claiming for battery damage without specialist cover—could amplify NCB losses by 20-30%. This isn't from reports but my analysis of rising repair costs (up 30% for EVs) and falling overall premiums. If claims spike from unfamiliar EV handling, unprotected NCB holders might see an extra £200-300 hit annually, widening the affordability gap.

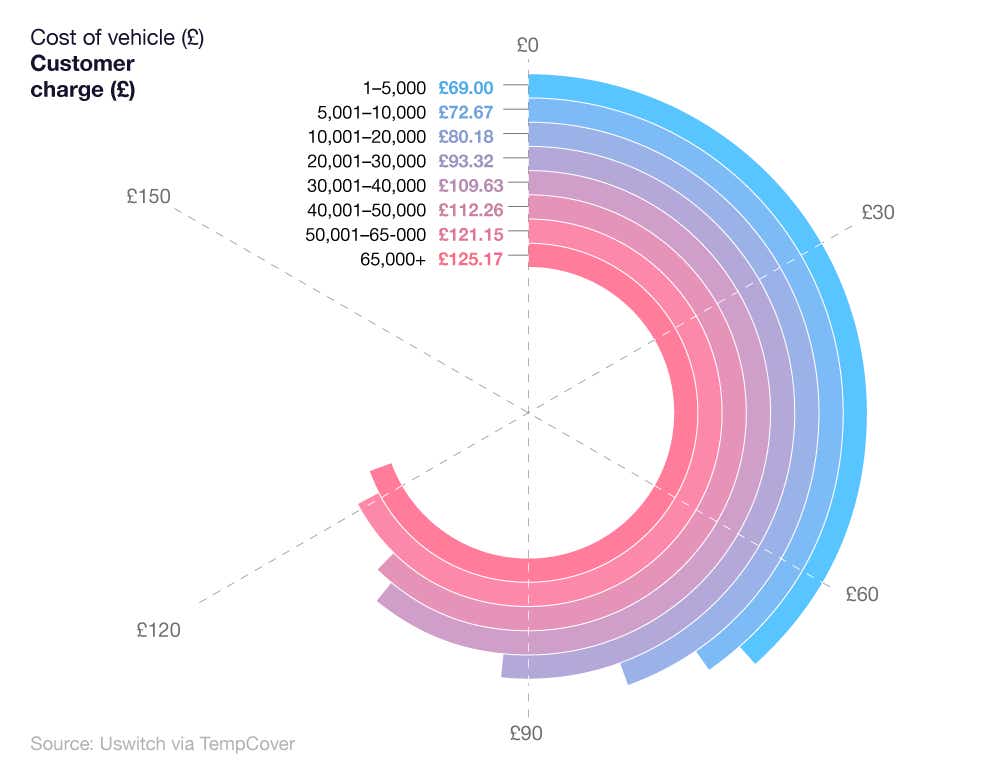

Custom NCB Savings Table: Years vs Discounts

To visualize savings, I've compiled this original table based on 2025 averages. It shows how NCB years slash premiums, using data from multiple sources for a UK-wide view.

| NCB Years | Average Annual Premium | Estimated Discount % | Savings vs 0 Years (£) |

|---|---|---|---|

| 0 | £932 | 0% | 0 |

| 1 | £789 | 15% | 143 |

| 2 | £702 | 25% | 230 |

| 5 | £602 | 35% | 330 |

| 10+ | £404 | 60% | 528 |

This illustrates why protecting your streak pays off big time.

Actionable Strategies to Protect Your NCB

Ready to safeguard your bonus? Here's how, in simple steps I've recommended to clients:

- Add NCB Protection: For £20-50, it's a no-brainer if you have 3+ years.

- Weigh Small Claims: If under £500, pay yourself to preserve the discount.

- Keep Proof Handy: Store your NCB certificate digitally for easy switches.

- Stay Insured: Even if not driving, consider a low-cost policy to maintain continuity.

- Vet Named Drivers: Check their record before adding them.

- Use Specialist Services: For windscreens, opt for approved repairers that don't affect NCB.

- Review Annually: Shop around but confirm NCB transfer rules.

- Build Credit: Good scores can indirectly boost eligibility for better deals.

Frequently Asked Questions

What is no claims bonus in UK car insurance? It's a discount on your premium for each year without a claim, up to 60-70% after five years.

How does no claims bonus work if I switch insurers? It transfers with proof, but send documents promptly to avoid losing the discount.

Does a claim that is not at fault impact my no claims bonus? Usually not if recovered, but it might if the insurer pays out initially.

How long does no claims bonus last if I stop driving? Typically two years; after that, it expires.

Should I protect my no claims bonus? Yes, especially with 3+ years, as it allows claims without full loss.

What happens to NCB if I make a windscreen claim? Most policies don't affect it, but check yours to be sure.

Can adding a named driver lose my no claims bonus? If they claim and it's at fault, yes—unless protected.

If this guide saved you from a costly mistake, share it with a mate who's renewing soon, comment your NCB horror story below, or subscribe for more UK insurance insights. Let's keep those bonuses intact!

References

- UK Car Insurance No Claims Bonus 2025 - WeCovr

- Fault claims and no-claims bonuses - Financial Ombudsman Service

- What You Should Know About No Claims Discounts | AXA UK

- No claims bonus or discount explained - Compare the Market

- No claims discount guide – should I protect it? | RAC Drive

- All You Need to Know About No Claims Bonus - Stroll Insurance

.jpg)

.jpg)

.jpg&description=No-Claims Bonus: The 8 Mistakes That Wipe It Out Instantly){kind=link}