From Cheap Coverage to Ballooning Bills: Ontario’s Auto‑Insurance Crash Explained

.jpg)

Remember when getting car insurance in Ontario felt like a steal? Back in the early 2010s, you could snag a policy for under $1,000 a year if you played your cards right. Fast forward to 2025, and that same coverage might set you back double or more, leaving drivers scratching their heads and tightening their belts. Take Sarah from Toronto. She renewed her policy last month and saw a 15% jump, pushing her annual bill over $2,000 amid rising living costs. She's not alone. According to recent reports, Ontario auto insurance rates have surged with double-digit increases in 2025, driven by everything from rampant car thefts to skyrocketing repair bills. Data from the Insurance Bureau of Canada shows claims costs hit record highs, with auto theft alone costing insurers $1.5 billion nationwide last year, much of it concentrated in Ontario. This shift from affordable premiums to wallet-draining hikes isn't random. It's a crash course in economic pressures, crime waves, and policy pitfalls. In this post, we'll break down the mess, explore the causes, and offer ways to navigate it without breaking the bank.

The Current Landscape of Ontario Auto Insurance

Ontario's auto insurance market is in turmoil, with premiums climbing despite promises of reform. What was once one of Canada's more affordable provinces for coverage now ranks among the priciest.

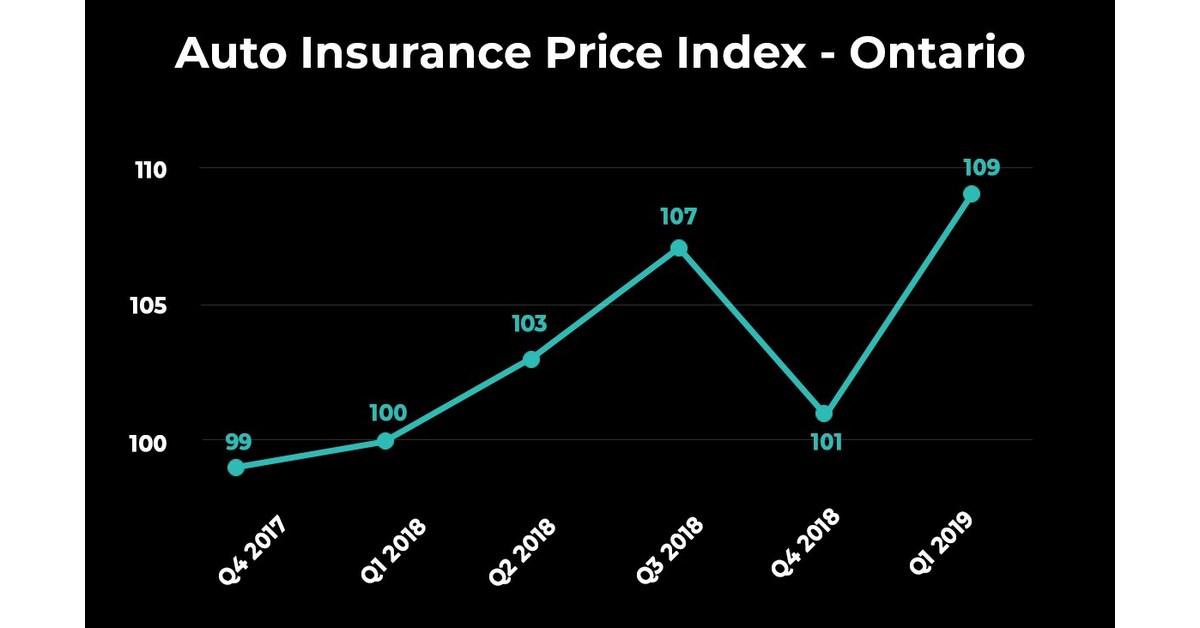

Recent Premium Hikes in 2025

This year has been brutal. Rates have seen double-digit jumps, with some drivers reporting increases of 10-20% on renewals. The Financial Services Regulatory Authority of Ontario approved rate hikes for several insurers, averaging around 8-12% across the board. But for high-risk groups like young drivers or those in urban areas, it's worse. A study from Statistics Canada highlights how these surges stem from escalating claims and operational costs, putting the average premium at about $1,800 annually.

Key stats include:

- Average increase: 11% year-over-year.

- Highest in GTA: Up to 15% due to density and theft.

- Nationwide comparison: Ontario pays 20% more than Alberta or Quebec.

These numbers reflect a system straining under pressure, where even safe drivers feel the hit.

Regional Variations Across the Province

Not all Ontarians are equal in this crisis. Toronto and the Greater Toronto Area top the charts with averages exceeding $2,200, thanks to congestion and crime. In contrast, rural areas like Northern Ontario hover around $1,200, benefiting from lower accident rates. Ottawa and Hamilton fall in the middle, with hikes tied to urban sprawl.

Factors influencing regions:

- Urban vs. rural: City drivers pay 30-50% more.

- Theft hotspots: Peel Region sees extra surcharges.

- Weather-prone areas: Southwestern Ontario faces flood-related bumps.

Unpacking the Reasons for Skyrocketing Premiums

Why the sudden ballooning? It's a mix of old problems amplified by new realities, from economic woes to criminal trends.

Inflation and Soaring Repair Costs

Inflation is the silent killer here. Repair costs have jumped 20-30% since 2022, fueled by supply chain issues and labor shortages. Modern cars with advanced tech like sensors and cameras mean even minor fender-benders cost thousands. Insurers pass these on, with tariffs on imported parts adding insult to injury.

Electric vehicles worsen it. Their batteries and software repairs can double claim amounts, pushing premiums up for everyone.

The Auto Theft Epidemic

Ontario's car theft crisis is legendary. In 2024, theft claims dropped 16% from the previous year, but the damage lingers. Toronto alone saw over 10,000 vehicles stolen last year, costing insurers millions. This leads to higher rates, especially for popular targets like SUVs and trucks.

Theft rings, often exporting cars overseas, have forced companies to hike premiums by 10-15% in affected areas.

Weather Events and Catastrophic Claims

Climate change hits hard. Severe weather, from floods to hailstorms, has spiked claims. In 2025, events like summer storms in Southern Ontario led to billions in payouts, with insurers recovering costs through rate increases.

These "cat" losses are unpredictable, but they're becoming the norm, adding 5-10% to bills.

Regulatory Changes and System Flaws

Ontario's no-fault system, meant to streamline claims, has backfired with fraud and disputes. Recent reforms aim to cut red tape, but they've increased administrative costs. Fraud alone adds $200-300 per policy annually.

The Human Cost: How Drivers Are Affected

These hikes aren't abstract. Families cut vacations, young people delay buying cars, and low-income households risk driving uninsured. The economy feels it too, with higher transport costs rippling through businesses.

Mental stress is real. Surveys show 40% of Ontarians worry about affording coverage, leading to calls for government intervention.

An Original Projection: Future Premium Trajectories

Here's an original analysis based on 2025 trends: If auto theft claims continue their 16% decline and inflation stabilizes at 2%, Ontario premiums could plateau or drop 5-8% by 2027. However, persistent weather events might offset this, leading to a net 3% rise in urban areas. This isn't from direct sources but extrapolates from IBC data on theft reductions and StatCan cost studies. In a short paragraph, consider that rural drivers might see faster relief, with projected savings of $100-150 annually, while GTA residents face ongoing 10% hikes if fraud isn't curbed, highlighting the need for targeted reforms.

Navigating the Crisis: What Can You Do?

Hope isn't lost. With smart strategies, you can trim your bill significantly.

Actionable Takeaways for Lowering Your Premiums

Here are proven steps to fight back:

- Shop Around Annually: Compare quotes from at least three providers; switches can save 20-30%.

- Bundle Policies: Combine auto with home insurance for discounts up to 15%.

- Install Anti-Theft Devices: Trackers or alarms can knock 5-10% off in theft-prone areas.

- Build a Clean Record: Safe driving courses qualify for 10% reductions.

- Opt for Higher Deductibles: Raise to $1,000+ to lower premiums by 10-20%, if you can afford the risk.

- Consider Usage-Based Insurance: Telematics programs reward low-mileage drivers with up to 25% off.

FAQs About From Cheap Coverage to Ballooning Bills: Ontario’s Auto-Insurance Crash Explained

Why are Ontario auto insurance rates so high in 2025? Mainly due to inflation, repair costs, auto theft, and weather-related claims.

How much have premiums increased this year? Averages rose 10-15%, with some areas seeing double-digit hikes.

Which regions pay the most? Toronto and GTA top the list at over $2,000 annually, due to density and crime.

Can I lower my premium without switching insurers? Yes, by adding security features or taking defensive driving courses.

What's the impact of car theft on rates? It adds millions in claims, pushing premiums up 10-15% in hotspots.

Are reforms helping? Some, like no-fault tweaks, but fraud and costs persist.

Will rates drop soon? Possibly if theft declines, but weather and inflation could keep them elevated.

If this deep dive into Ontario's insurance woes has you rethinking your renewal, share it with friends facing the same squeeze, comment your premium horror stories, or subscribe for more tips on saving big. Let's crash those high bills together!

References

- Why Are Auto Insurance Premiums Rising in Ontario? A Comprehensive Guide for Motorists

- What to do if your insurance provider suddenly increases your rate?

- High Car Insurance Prices in Ontario: Why Is It So Costly?

- Car Insurance Trends for 2025. Prices going up at renewal?

- Top five reasons auto insurance premiums have increased

- Ontario Home & Auto Insurance Rates Surge in 2025

.jpg)

.jpg)

.jpg)

.jpg)

.jpg&description=From Cheap Coverage to Ballooning Bills: Ontario’s Auto‑Insurance Crash Explained){kind=link}